What Are VA Loans?

As the video says, the name is misleading - they’re not loans FROM the VA.

The VA - short for “US Department of Veterans Affairs” - is the Federal military veteran benefit system.

The VA administers benefits and services for Servicemembers, Veterans their dependents and survivors.

Programs related to home loans are one of their key services.

The VA is not a bank; they do not provide home loans themselves.

But they do guarantee a portion of home loans provided to veterans and other eligible people by banks and mortgage companies.

These guarantees enable lenders to provide more favorable terms.

They are are commonly called “VA Loans”.

They cover buying, building, repairing, retaining and adapting homes for personal occupancy by eligible Veterans and survivors.

The most common FHA program is the 203(b) FHA Loan. It offers a low down payment, flexible qualifying guidelines limited lender's fees, and a maximum loan amount.

A 203(k) loan enables a home buyer to finance both the purchase and rehabilitation of a home through a single mortgage. A portion of the loan is used to pay off the seller's existing mortgage and the remainder is placed in an escrow account and released as rehabilitation is completed.

Basic guidelines for 203(k) loans are as follows:

The 203(k) loan must follow many of the 203(b) eligibility requirements. Lenders will know specifics about improvement, energy efficiency, and structural guidelines.

While this video simplifies things to help you remember, except for the addition of an FHA mortgage insurance premium, FHA closing costs are similar to those of a conventional loan.

As of 2013, the FHA requires a single, upfront mortgage insurance premium equal to 2.25% of the mortgage to be paid at closing (or 1.75% if you complete the HELP program).

This initial premium may be partially refunded if the loan is paid in full during the first seven years of the loan term.

After closing, you will then be responsible for an annual premium - paid monthly - if your mortgage is over 15 years or if you have a 15-year loan with an LTV greater than 90%.

The video explains the steps in FHA loans in more visual terms. With the exception of a few additional forms, the FHA loan application process is similar to that of a conventional loan.

With new automation measures FHA loans may be originated more quickly than before. And, if you don't prefer a face-to-face meeting, you can apply for an FHA loan via mail, telephone, the Internet, or video conference.

Remember these points from the video:

In fact, an FHA down payment could be as little as a few months rent. And your monthly payments may not be much more than rent.

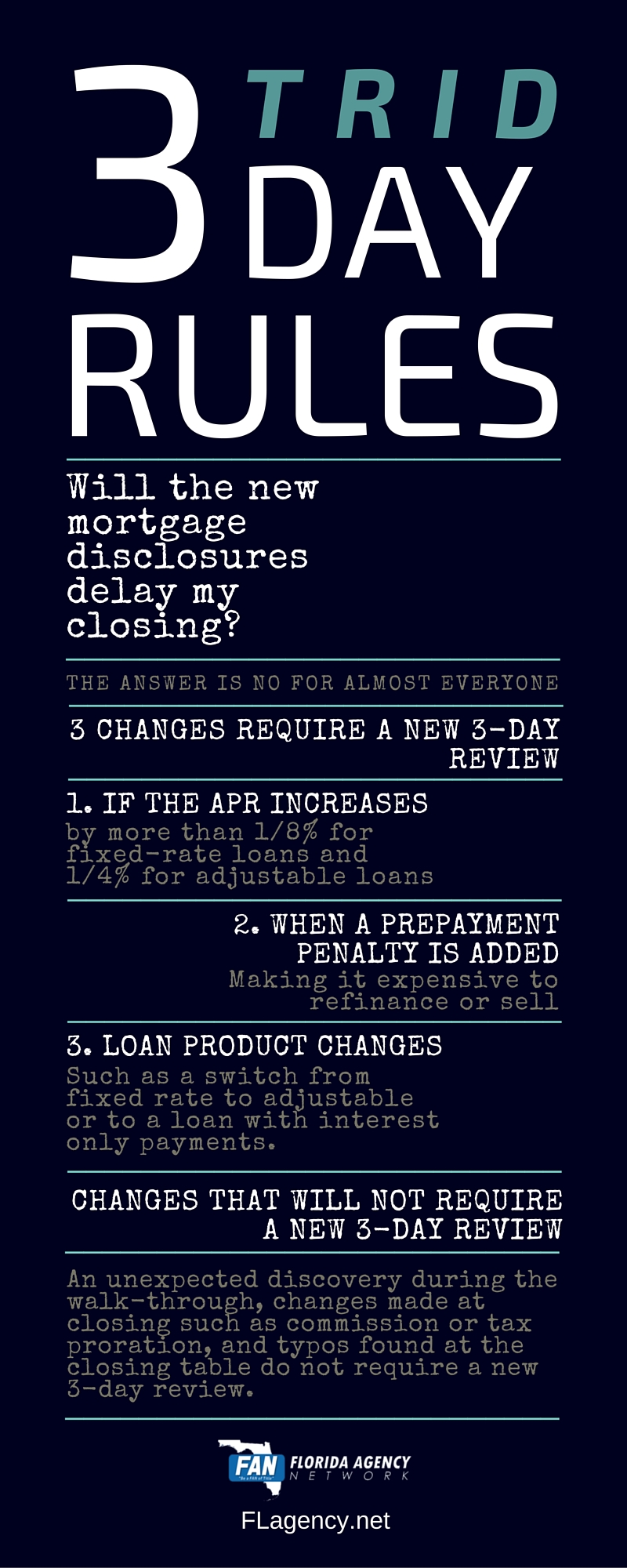

One of the regulations associated with the new TRID forms is a 3-day rule. The 3-Day rule mandates borrowers MUST receive the Closing Disclosure 3-days before the closing date. This new rule gives consumers the opportunity to review the closing disclosure and ensure all information is correct and correlates with the Loan Estimate.

However, what happens if any changes need to be made?

The infograph below explains three situations that would require a new closing disclosure and thus, delay your closing.

What you’ll see in this video is, there may be closing costs customary or unique to a certain locality but closing costs are usually made up of the following:

And any documentation preparation fees.

Compliance is the new normal and the Florida Agency Network is leading the way.

With a SOC 1 Type 1 Examination under our belts, FAN is being recognized for its commitment to creating the highest quality security of services for our customers.

Check out our feature in The Title Report, by clicking here.

As we show you in this video:

And the keys to your new home!

Please fill out form below