In addition to the required pieces:

A creditor may collect whatever additional information they deem necessary.

However, as soon as you have provided the 6 required pieces, the creditor has 3 business days to provide a Loan Estimate for approved loans.

Submitting these 6 pieces of information:

constitutes a valid loan application under the TRID rule.

You may apply and submit these in writing OR in oral form; a live conversation, or a phone call, backed by a written record of the conversation is a legitimate application.

Once these 6 pieces of information are submitted a creditor MUST supply a Loan Estimate for approved loans within 3 business days.

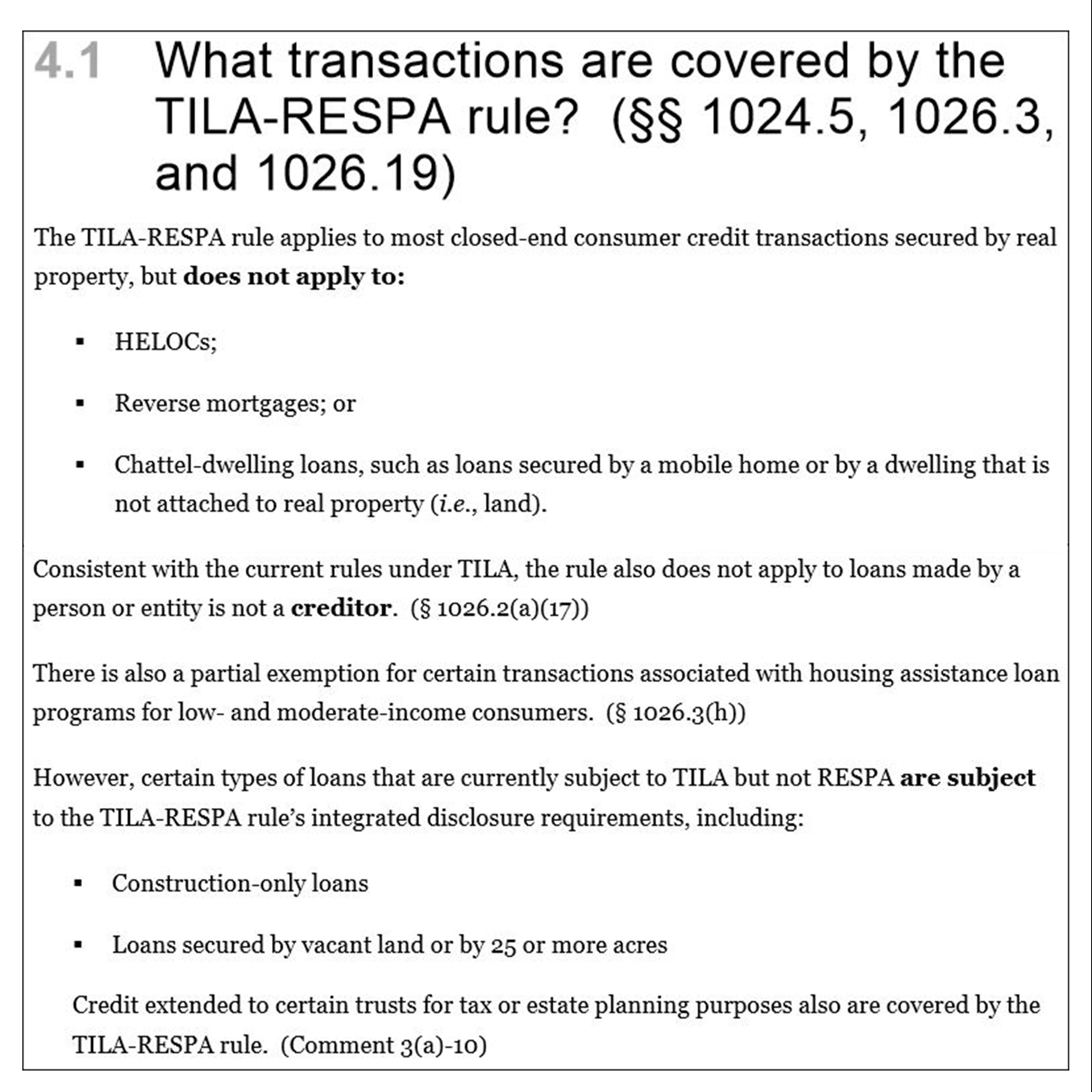

Creditors must continue to use the Good Faith Estimate, Truth-In-Lending Disclosure and the HUD-1 form for reverse mortgages, HELOCs, mobile home or other non-attached dwelling loans and others NOT covered by TRID.

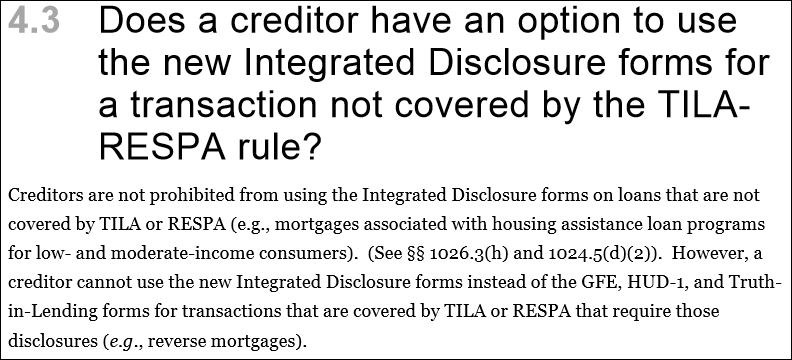

Housing assistance loans for low- and moderate-income consumers are partially exempt from TRID disclosures, and have specific rules.

Creditors are not required to provide Loan Estimate and Closing Disclosure forms and related booklets and statements for these loans.

TRID rules apply to MOST consumer credit transactions secured by real property. These include mortgages, refinancing, construction-only loans closed-end home-equity loans, and loans secured by vacant land or by 25 or more acres.

The rule does NOT apply to Home Equity Line of Credit transactions reverse mortgages mortgages secured by a mobile home or other dwelling that is not attached to real property.

Also, TRID rules do NOT apply to loans made by a person or business that makes 5 or fewer mortgages in a calendar year.

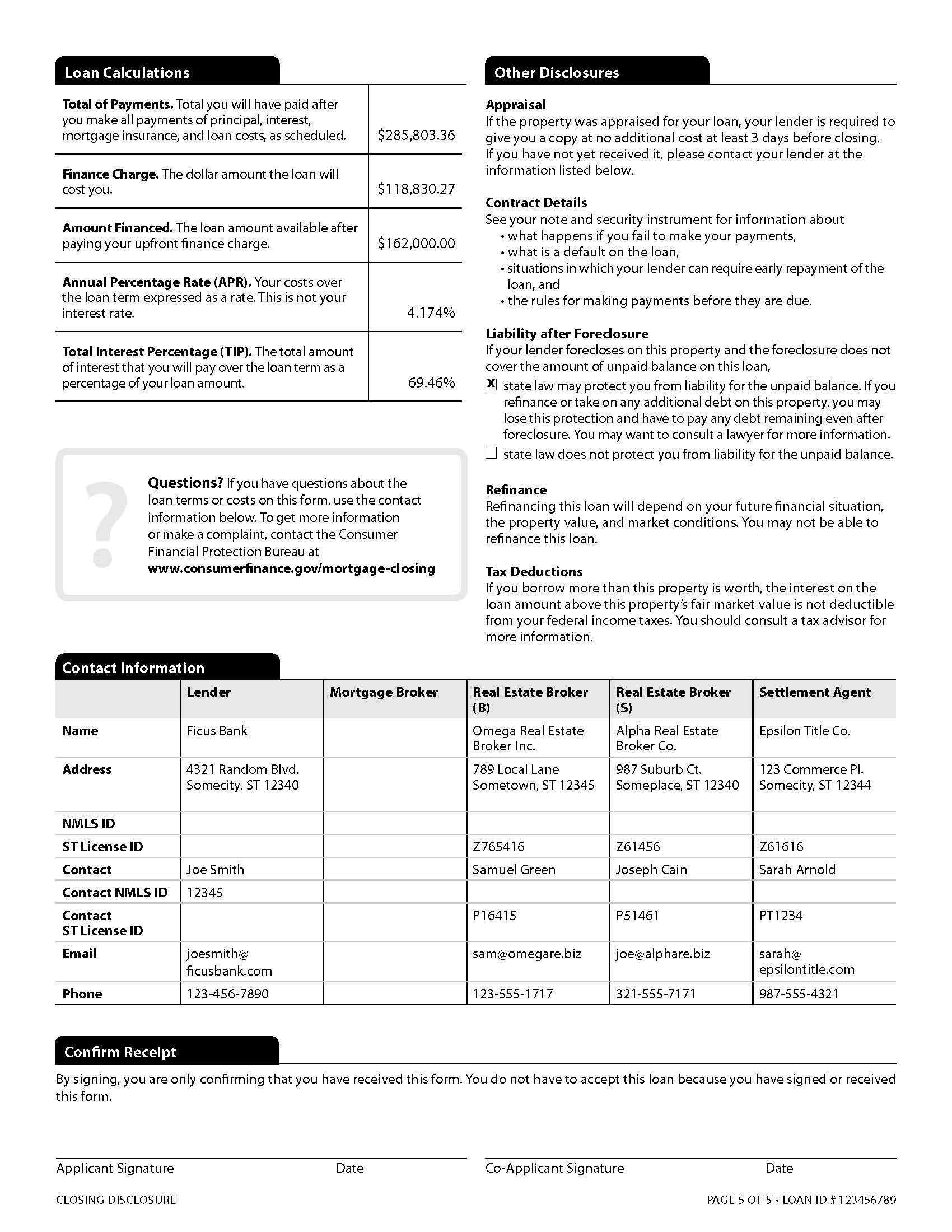

Federal “disclosure” forms define the information that creditor businesses MUST provide to consumers applying for real estate loans.

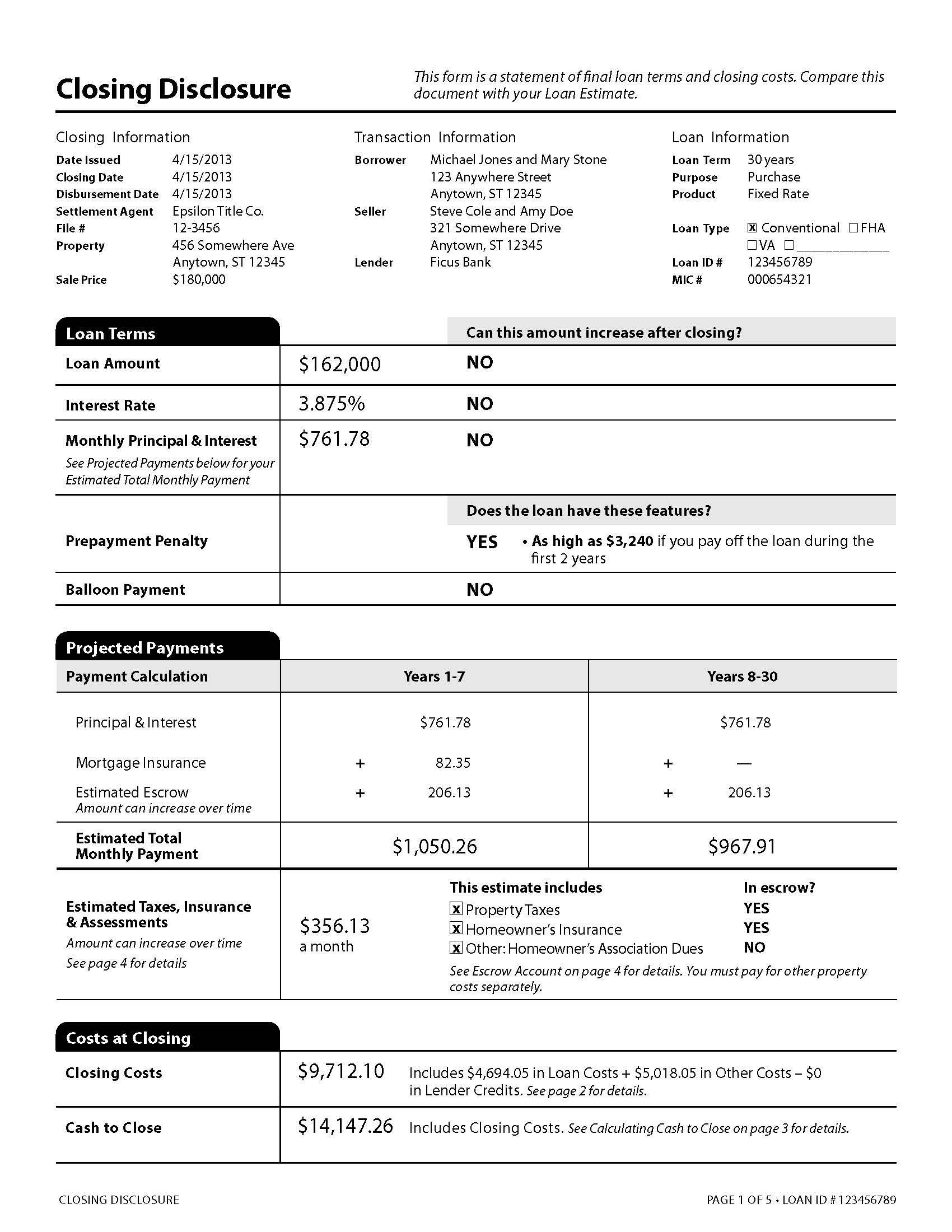

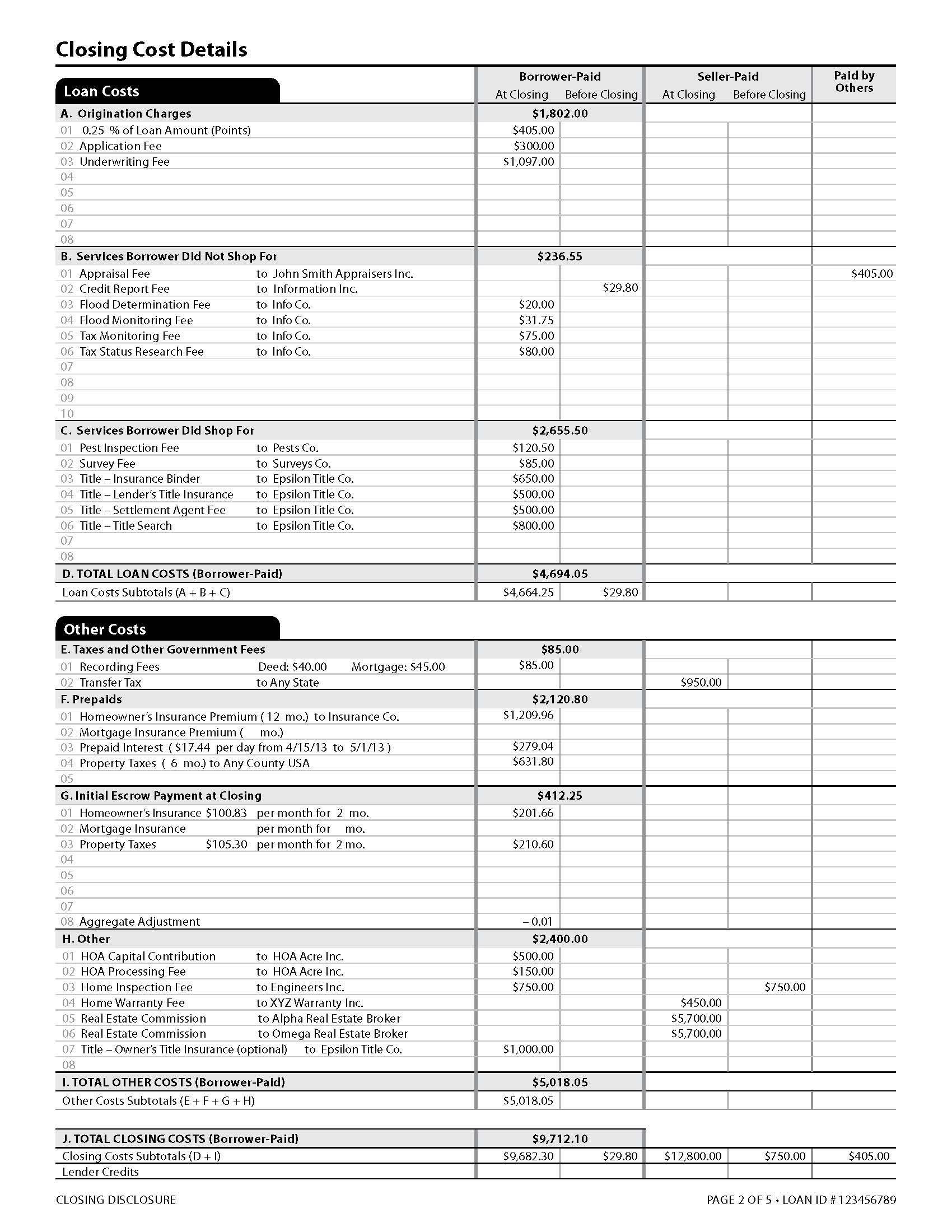

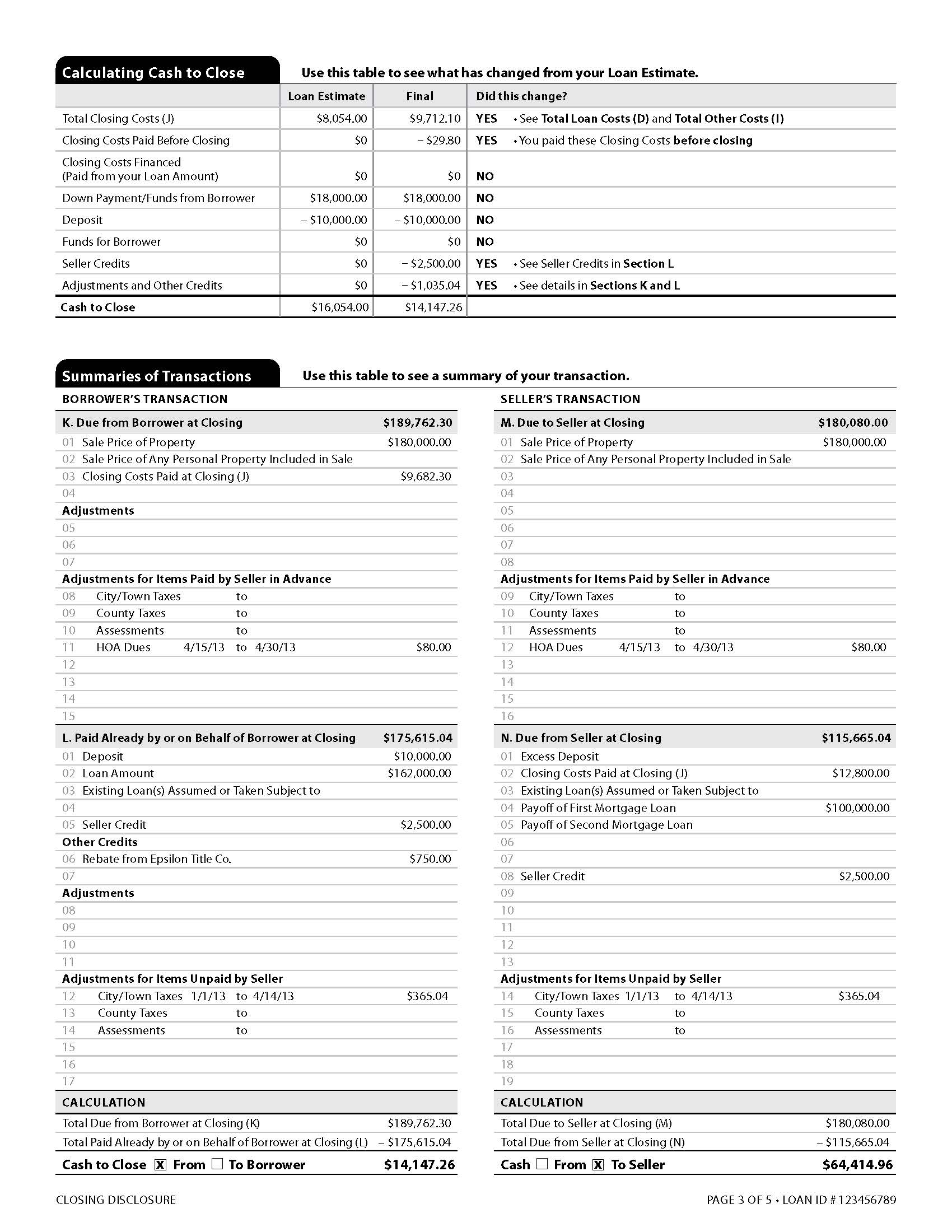

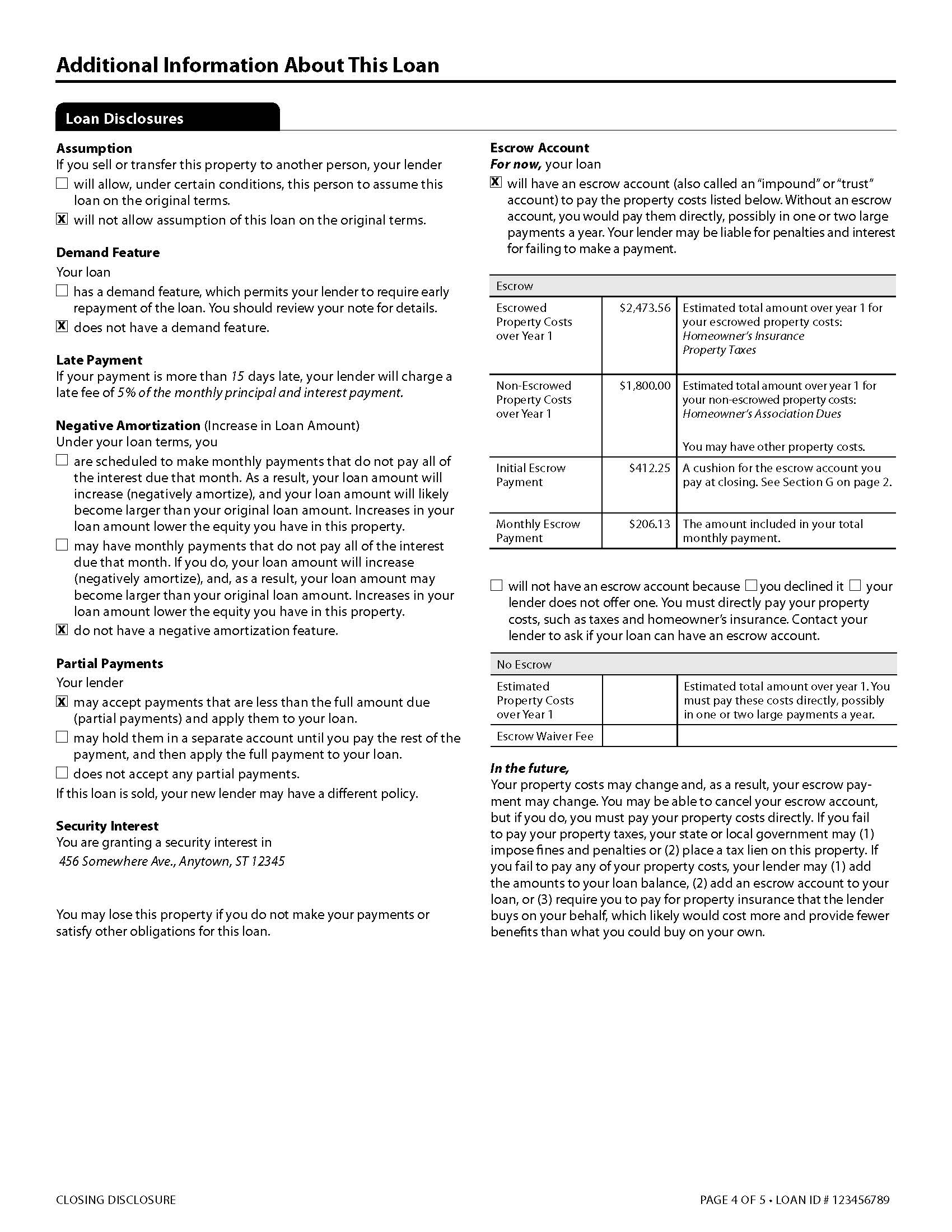

As of Oct 1, 2015 lenders must provide TWO New “TRID” disclosure forms. for the most common kinds of real estate loans First, the Loan Estimate, which covers the key features, costs and risks of a mortgage loan.

For an approved loan this must be returned to the consumer within 3 business days of loan application. If the loan goes forward, the Closing Disclosure form, covering key transaction costs, must be delivered at least 3 business days before loan consummation.

After October 3, 2015 you will no longer be receiving a HUD-1 settlement statement before consummation of a closed-end credit transaction secured by real property.

Say what?!?!

That's right, I just said consummation of a closed-end credit transaction and no more HUD. There is new jargon to go along with the new, easy-to-read, consumer friendly, disclosures.

Bon Voyage HUD!

Take a peek at the new disclosures!

www.closing-disclosure.com

2015 Florida Realtors® Convention & Trade Expo

Each year, the Florida Realtors® Convention & Trade Expo gathers thousands of Realtors looking to up their game. This years theme is Celebration 15; the event falls on August 19-23 and is held at the Rosen Shingle Creek in Orlando, Florida. The free two-day Expo is on Thursday and Friday--all you have to do is register. There are over 30 education sessions sorted into six learning tracks--technology, broker, productivity, trends, personal growth, and continuing education. Along with the Convention, the Trade Expo has over 200 exhibitors that come packed with promotional materials and exquisite raffle prizes. This years keynote speaker is Notre Dame's former Head Coach Lou Holtz.

On October 3, 2015 the TILA-RESPA Integrated Disclosure (TRID) rule will go into effect. The Florida Agency Network (FAN) is leading the industry through uncharted waters to the new disclosures. Title agencies in the FAN network are prepped and ready to keep you afloat before, during, and after these industry changes. Join us at booth 625 as we say Bon Voyage to the HUD-1 and celebrate the implementation of the new Closing Disclosure (CD). Get social with us and enter to win an Apple iWatch!

Stay on top of your game by familiarizing yourself with the general requirements that are going change in regards to the Good-Faith Estimate when the new TILA-RESPA Integrated Disclosure (TRID) rule goes into effect.

First of all, it is no longer going to be called a Good-Faith Estimate but will then be identified as a Loan Estimate.

Guess what?!?!

The jargon isn't the only thing that is changing! The new disclosure carries with it some timing deadlines as well as a new look and lay out to the forms used instead of the familiar GFE.

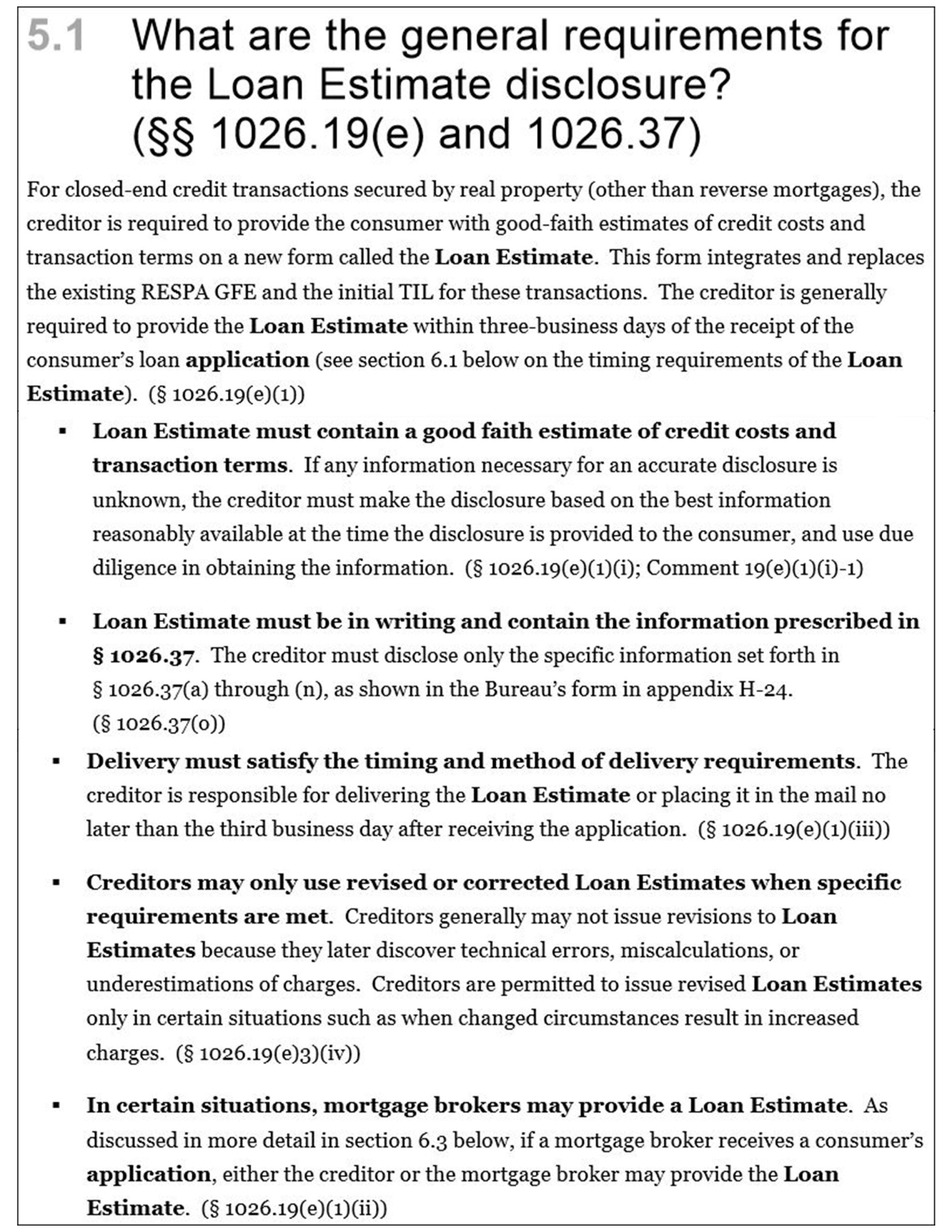

The creditor, formally known as the lender, is required to provide all consumers of closed-end transactions secured by real property with a good-faith estimate of credit costs and transaction terms.

Mortgage brokers or creditors may provide the Loan Estimate to the consumer when the mortgage broker receives the consumer's completed application and must be provided no later than 3 business days after the completed application has been turned in.

This new TILA-RESPA form integrates and replaces the current RESPA GFE and the initial TIL for these transaction types. Creditors must issue a revised Loan Estimate only in situations where changed circumstances resulted in increased charges.

These general requirement changes are meant to help better inform, protect and serve the consumer. The Florida Agency Network is ready to guide the industry through these changes and looks forward to partnering with you to streamline the process.

Schedule a Training Class

The TILA-RESPA rule (TRID) is proposed to go into effect this year on October 3. Buyer's Agents will need to be aware of 3 main things: what type of loan product their client is using to purchase, the expected closing date and if their title partner is approved to do business with their client's lender of choice. This is especially true when it comes down to writing the contract.

Not all Transactions are Covered by the New Rule

Not all Transactions are Covered by the New Rule

Most closed-end consumer credit transactions that are secured by real property are covered by the new rule.

Certain types of loans that are currently subject to TILA but not RESPA are subject to the TRID rule as well, such as construction-only loans, loans secured by vacant land or by 25 or more acres and credit extended to specific trusts for estate planning purposes.

TRID will not cover HELOC's, Reverse Mortgages or Chattel-dwelling loans. Other exemptions include loans that are made by a person or entity that makes five or fewer mortgages in a calendar year. In addition to, housing assistance loan programs for low- and moderate- income consumers are partially exempt.

It's All About Timing

The typical timeline of the closing process is going to change not only in the form of new documents and disclosures but on the operational side of things as well. It will take some time for the industry to adjust to these changes. Just after the rule goes into effect, it is recommended to add on an extra 15 days to the closing date when writing the contract. Eventually, as the industry adjusts, the forecast predicts this will move us to a more paperless environment resulting in an even quicker closing timeline of less than the typical 30 days in Florida.

Is Your Title Partner Approved to do Business With Your Client's Lender?

Is Your Title Partner Approved to do Business With Your Client's Lender?

Security is the main issue in regards to compliance between Title Agencies and Lenders due to the obligation both parties must protect Non-Public Information (NPI) data that is exchanged during a transaction. Lenders cannot do business with agencies that do not have compliant software to protect NPI. Technology has a big role in securing data. In an effort to comply, Agencies in the Florida Agency Network use SoftPro to secure the communication of NPI. You can find SoftPro on the American Land and Title Association's Elite List of 12 Providers that can assist with compliance.

It is best to work with a preferred title partner that is compliant to ensure the least amount of hicups at the closing table. FAN has multiple agencies in our network that are ready to take on these changes. To find an agency in the network near you visit www.flagency.net or contact Max@FLagency.net.

Check out what the CFPB has to say below or visit their site by clicking here:

Please fill out form below