Yes. Like the video shows, lenders now offer several affordable mortgage options which can help first-time homebuyers overcome obstacles that made purchasing a home difficult in the past.

Lenders may now be able to help borrowers who don't have a lot of money saved for the down payment and closing costs, have no or a poor credit history, have quite a bit of long-term debt, or who have experienced income irregularities.

What are the “Ability to repay” rules about?

In a nutshell, as this video shows, new laws require lenders to make a good-faith assessment of a borrower’s capacity to pay back their loan over time.

It’s a longer-term view that goes beyond immediate income, debt and credit rating.

These new Federal laws- supervised by the CFPB - require lenders to ask more questions - about income, assets, employment, credit history, and monthly expenses - as they relate to the proposed loan.

For example, a lender offering a mortgage with a low initial rate must try to assess how a borrower will handle the later, higher rate as well.

If you’re applying to borrow ask whether the program you’re considering is a Qualified Mortgage

Ability-to-repay rules are built in to loans that meet Qualified Mortgage guidelines.

There are mortgage options now available that only require a down payment of 5% or less of the purchase price. You’ll see some pictures in this video to help you remember later - the larger the down payment, the less you have to borrow and the more equity you'll have.

Mortgages with less than a 20% down payment generally require a mortgage insurance policy to secure the loan.

When considering the size of your down payment consider that you'll also need money for closing costs moving expenses, and - possibly - repairs and decorating.

While this video simplifies things to help you remember, the loan to value ratio is the amount of money you borrow compared with the price or appraised value of the home you are purchasing.

Each loan has a specific LTV limit. For example: With a 75% LTV loan on a home priced at $100,000 you could borrow up to $75,000 (75% of $100,000) and would have to pay $25000 as a down payment.

The LTV ratio reflects the amount of equity borrowers have in their homes. The higher the LTV the less cash homebuyers are required to pay out of their own funds.

So, to protect lenders against potential loss in case of default, higher LTV loans (80% or more) usually require mortgage insurance policies.

As this video explains, Federal laws put into effect in 2014 and supervised by the Consumer Financial Protection Bureau define lending practices and loan terms for a new category called “Qualified Mortgages.”

They provide stable loan features for consumers and improve legal protection for lenders who follow the guidelines.

These guidelines require lenders to assess each borrower’s ability to repay their mortgage loan.

As of 2014, guidelines require that a borrower’s monthly DEBT - including mortgage - be no higher than 43% of their monthly gross INCOME.

The laws also define unacceptable loan terms:

The laws aim to provide consumers with objective guidance about reasonable debt from the CFPB and in return, to grant lenders who follow that guidance with higher levels of protection from lawsuits.

Ask your lender about Qualified Mortgage options for your home purchase.

The original phrase “mort gage” translates as “death pledge”! But as this video explains, a mortgage is a loan obtained to purchase real estate.

The "mortgage" itself is a lien - a legal claim on the home or property that secures the promise to pay the debt.

All mortgages have two features in common: principal and interest.

The principal is the amount you are borrowing which is “secured” by the lender’s claim on the property.

The interest, usually stated as the percentage rate is the additional amount paid for borrowing. Mortgage interest is ‘compounded’ - interest on interest, over time.

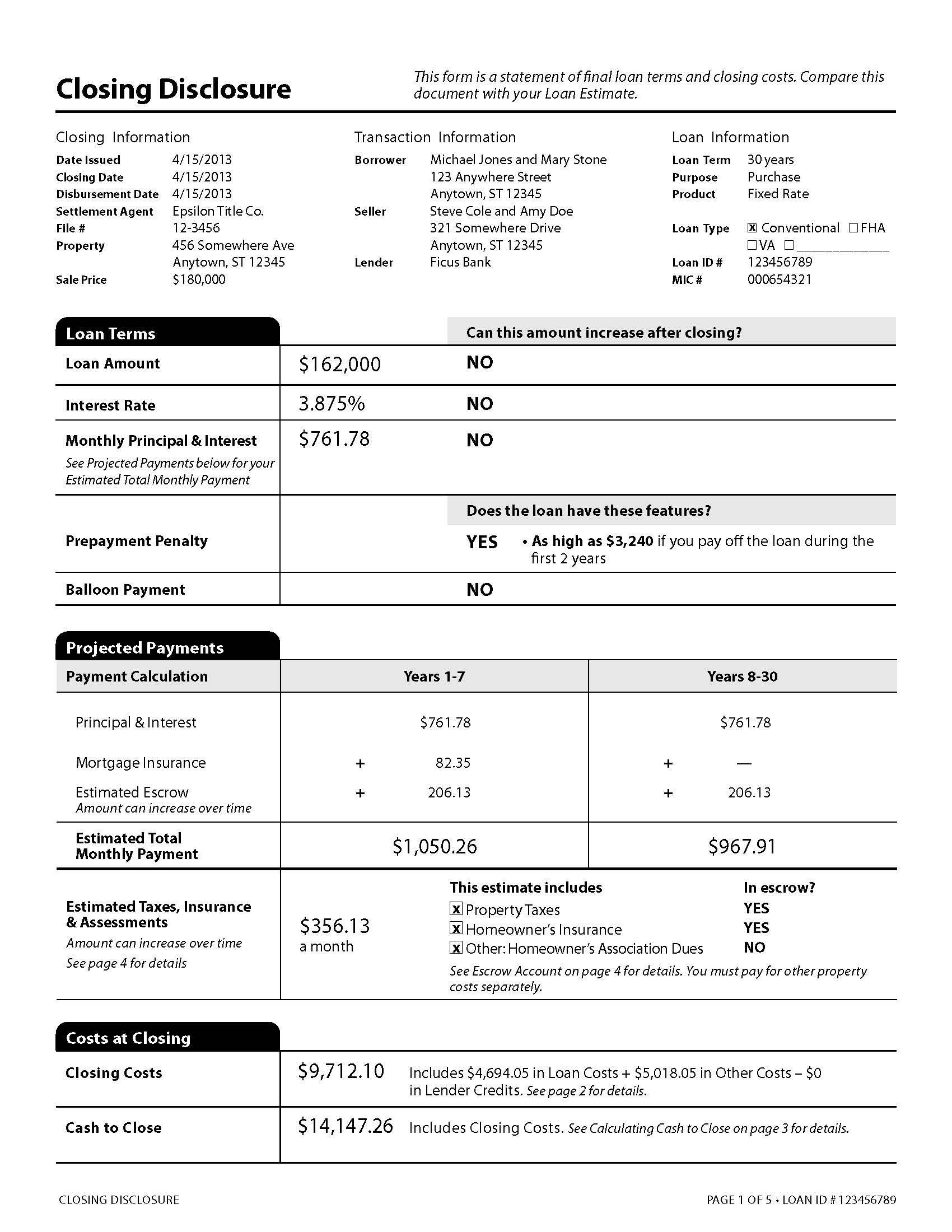

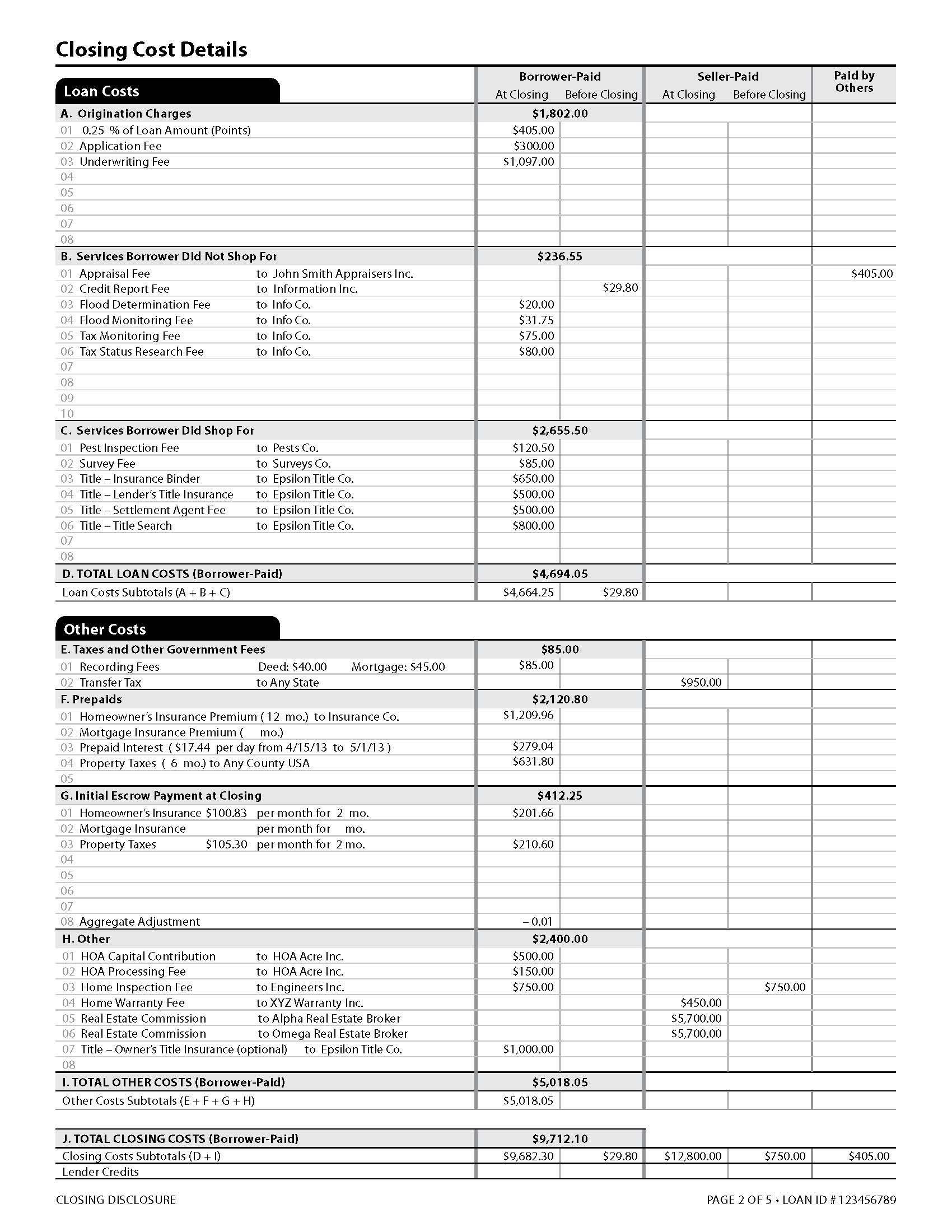

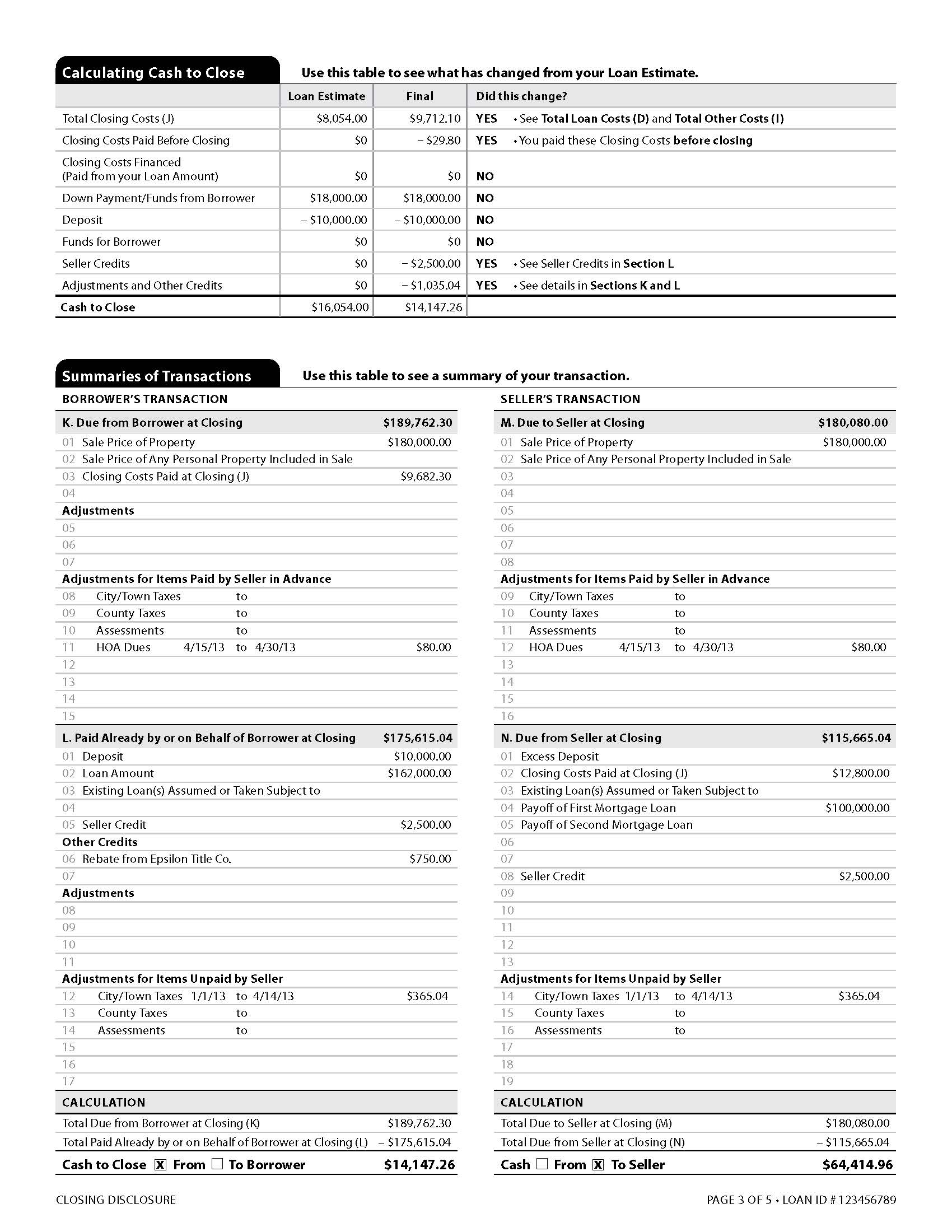

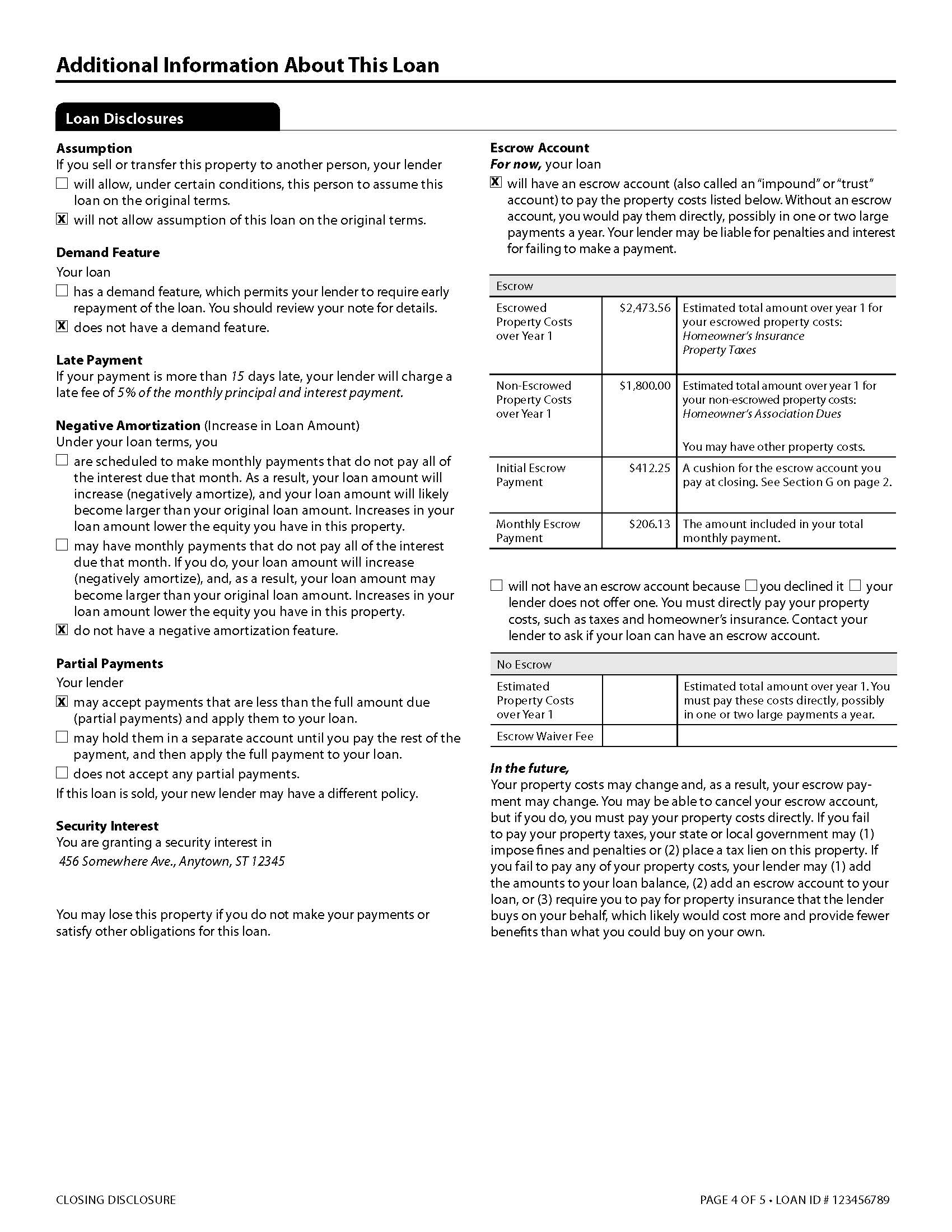

After October 3, 2015 you will no longer be receiving a HUD-1 settlement statement before consummation of a closed-end credit transaction secured by real property.

Say what?!?!

That's right, I just said consummation of a closed-end credit transaction and no more HUD. There is new jargon to go along with the new, easy-to-read, consumer friendly, disclosures.

Bon Voyage HUD!

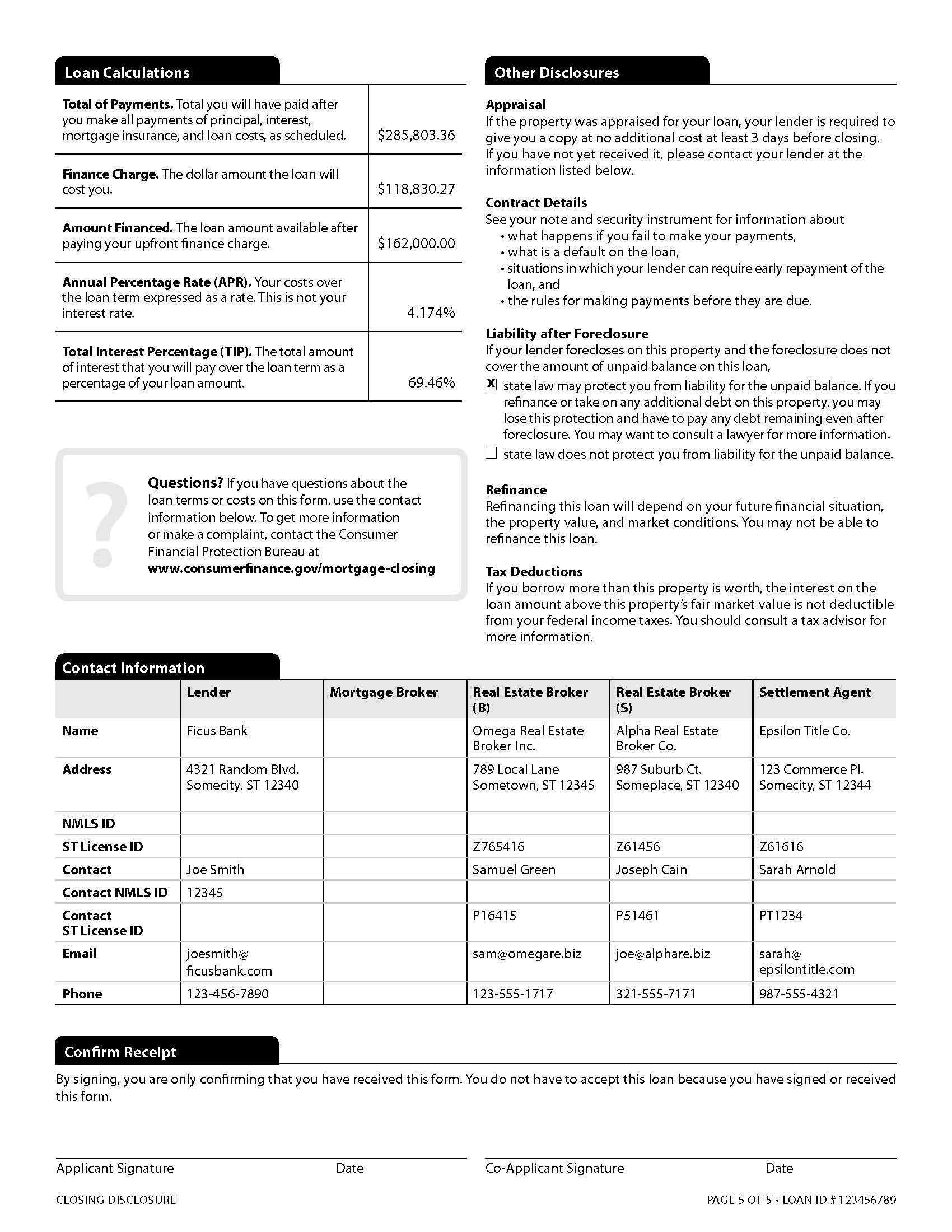

Take a peek at the new disclosures!

www.closing-disclosure.com

Please fill out form below